Most adults are familiar with the concept of a personal credit score, but did you know that businesses have a separate credit score that lenders use to evaluate when a business needs funding? The two credit scores should be kept separate, so your personal score is not impacted by debts your business takes on and vice versa. Here, we will explain how your business credit score works and why it is important.

What is a Business Credit Score

You have your personal credit score, which is what is used when you want to open a new credit card, buy a home or car, or take out a personal loan. Your business credit score can be used for similar things, like obtaining a business loan or a business credit card. Like with the personal credit score, your business credit score is built up by paying your bills and loans on time.

Is Your Personal and Business Credit Score the Same Thing?

Your personal credit is the history of you personally, going back to the first time you took out a line of credit in some way, whether your first credit card, mortgage, student loans, car payments, or something else. Your Social Security number (SSN) is linked to your personal credit score, and your credit transactions are compiled by the three credit bureaus, who then calculate it to determine your credit score.

A business credit score is for any credit transactions you do in the name of your business. Business credit functions similarly to personal credit, but there are some key differences. A business credit score is linked to its Employee Identification Number (EIN). Your business credit transactions are linked to your EIN and collected by three credit bureaus to calculate your business credit score.

.jpg)

The Factors that Determine Business Credit Scores

There are a few factors that are used to calculate your business credit score. Each credit bureau does things somewhat differently, though, so some things may not be used at or may not be as important to one bureau as they are to another. The components used to calculate a business credit score include:

- Payment History: Does your business always make its payments on time? Paying bills late is one of the biggest things that can impact your business credit score.

- Age of Credit History: How long your business has been open and has been building its credit score.

- Industry Risk: Some industries, like restaurants, are at a higher risk, and that can impact your score.

- Public Records: UCC filings and other similar records.

- Revenue: Higher profits can increase your credit score.

- Credit Limit: If you have over 25 percent of your credit limit currently spent, it can raise your score.

The most important thing that is looked at when calculating a business credit score is if your business pays its bills on time. All credit bureaus look at that, and sometimes that is the main thing that is part of determining your business credit score. Managing your debt is one of the key factors in credit scores, both business and personal.

What is a Good Business Credit Score

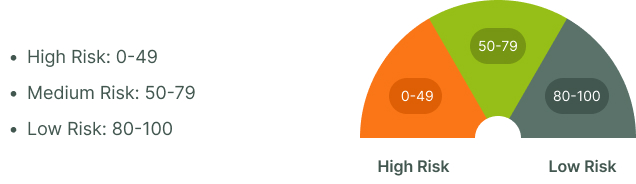

A personal credit score ranges from 350 to 850; the higher, the better. A business credit score is on a scale of zero to 100; the higher, the better. A good business credit score is anything above 80. With a high business credit score, you will have access to better loan terms and interest rates, and higher loan amounts will be available. Experian — one of the business credit score bureaus — breaks it down based on risk:

How Are Business Credit Scores Used?

If you need a loan for your business or want a credit card or line of credit, your lender will want your credit score. While you can use your personal credit score for this, you will need a high score to obtain the loan. With a business credit score, it can be easier for you to take out a business loan or line of credit. You will also have access to better loan terms and interest rates, as well as potentially lower insurance on the loans.

What is a Business Credit Report?

Your business credit report is a full report from the business credit bureaus that includes all of the information they have collected on your business to determine your creditworthiness of getting a loan or line of credit. In addition to the factors we mentioned above, other information on the credit reports can include details about your company, like the number of employees, subsidiaries, sales, and more. It lists every credit-related transaction, so you can use the report to find inaccuracies to help protect your credit.

How Can You Get Your Business Credit Report and Score?

You can check your business credit score by reaching out to the three business credit bureaus directly.

Unfortunately, unlike personal credit, business credit cannot be checked for free. However, Dun & Bradstreet does offer a free CreditSignal account, but this will not give you unlimited access to your credit report. Instead, you will have a monthly summary of your business credit transactions so that you can watch for any irregularities. We recommend that you be wary of any other free business credit report monitoring options; there are many scams out there.

How Do I Monitor My Business Credit Score?

We recommend that you check your business credit score a few times per year. The best practice is to check it at the beginning of each quarter. If you plan to take out a loan for your business, we recommend checking it a little more often to keep a better eye on it. While it can be time-consuming, the payout is a bigger loan with more favorable terms, which makes it well worth the effort. You can check your business credit score and report at the sites listed above.

When reviewing your business credit report, if you find an error, you can dispute it. The first thing to do is to check your reports from the other bureaus to see if the error is only on one report. If it is, this suggests that the error is on the bureaus side. In this case, contact the bureau with the error about it. You might have to provide proof, like showing that a payment was made on time. It can take weeks for an error to be removed from your credit report, which is why it is so important to monitor your business credit report. It can be harder for you to spot an error if you only check your credit once a year since there is so much information to comb through in a credit report.

How Can I Improve My Business Credit Score?

If your business credit score is lower than you would like it to be, you can build better business credit. A few things you can do to improve your business credit score are:

- Establish trade credit with suppliers: Paying your invoices on time from your suppliers helps you create a good credit history. Not all of your suppliers may be reporting your transaction history to the credit bureaus, but you can ask them to do so, which will help build your credit.

- Business credit card: Instead of using a personal credit card for business expenses, open a business credit card for those. Using the card and making payments on time can build up your business credit.Pay on time: Always make your payments on time, no matter who they are for. Overdue bills can hurt your business credit score.

- Apply for loans: Having a business loan that you pay on time will help improve your score. However, be careful not to take on more debt than you can handle.

- Keep credit accounts open: Instead of closing an account when you pay off a credit card, leave it open. This will give you longer credit history.

It is important to note that it can take you at least a year to obtain good business credit. Unfortunately, since it requires a good history, you need to spend time building that history. Many loans and credit applications will require three years of credit history before a business can qualify for financing through them. We recommend taking steps to build your business credit as soon as possible.

Help Your Business Grow

Your business credit score can help you get the funding your business needs to grow and thrive, or it can keep you limited, depending on what the score is. By monitoring your business credit and working to keep it high, your business will have access to the funding resources it needs.

Loans and credit lines are not the only way that you can help your business grow, grants are an excellent option for any business, and unlike loans, you do not have to pay the money back. Fundid's Grant Marketplace has the resources you need to find potential grants your business may qualify for. Visit our Grant Marketplace today to find more resources to help your business grow.